The purpose of CfD is to incentivise investments in new low-carbon electricity generation in the UK by providing stability and predictability to future revenue streams.

The Government stated that: ‘we must decarbonise electricity generation and it is vital that we take action now to transform the UK permanently into a low-carbon economy and meet our 20 per cent renewable energy target by 2020 and our 80 per cent carbon reduction target by 2050. To put us on this latter trajectory, power sector emissions need to be largely decarbonised by the 2030s. At the heart of our strategy to deliver this transition is a new system of long-term contracts in the form of Contracts for Difference (CfD), providing clear, stable and predictable revenue streams for investors in low-carbon electricity generation.’

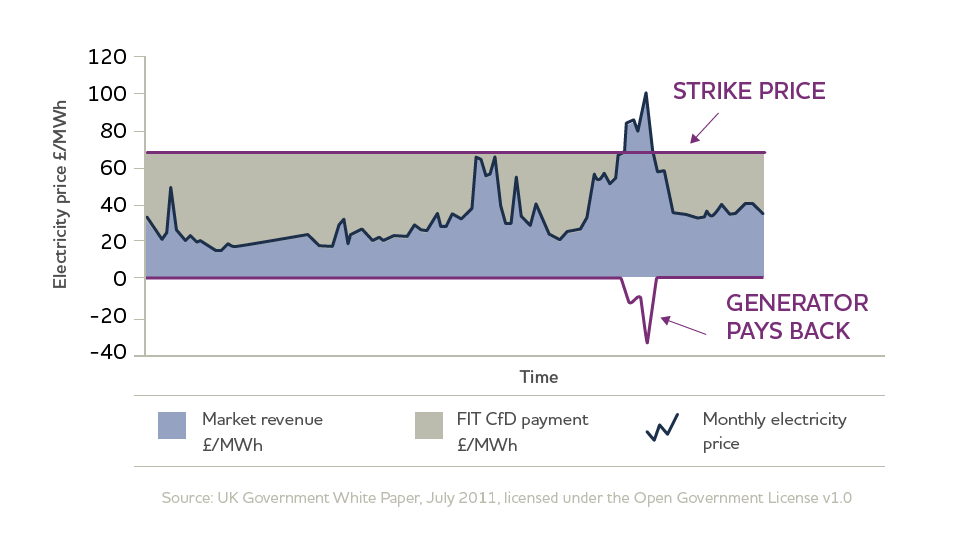

CfD explained

CfD is a long-term contract between an electricity generator and Low Carbon Contracts Company (LCCC). The contract enables the generator to stabilise its revenues at a pre-agreed level (the Strike Price) for the duration of the contract. Under the CfD, payments can flow from LCCC to the generator, and vice versa.

Under the CfDs, when the market price for electricity generated by a CfD Generator (the reference price) is below the Strike Price set out in the contract, payments are made by LCCC (see below) to the CfD Generator to make up the difference. However, when the reference price is above the Strike Price, the CfD Generator pays LCCC the difference. This is shown in the diagram below.

Supplier Obligation and Operational Costs Levy

The obligation to make payments to CfD Generators under CfDs (save for payments under investment contracts prior to the Supplier Obligation taking effect) will be funded by a statutory levy on all UK-based licensed electricity suppliers (Supplier Obligation). In addition, the operational costs of LCCC will be funded by a statutory levy on all UK-based licensed electricity suppliers (Operational Costs Levy). LCCC is responsible for collecting funds due from suppliers under the Supplier Obligation and the Operational Costs Levy.

The Supplier Obligation and Operational Costs Levy are set out in secondary legislation.

Our Role as CfD Settlement Services Provider

As Contract for Difference (CfD) Settlement Service Provider, it is our responsibility to run the CfD System and operate the processes that enable CfD payments to be calculated and settled.

This includes:

- Collecting metering data for CfD Generators.

- Managing settlement of payments by generators and suppliers

- Holding and managing reserve funds.

- Calculating payments and charges.

- Invoicing and collecting payments due.

- Maintaining the systems that allow us to collect, securely store, and where appropriate securely transmit the data necessary for CfD settlement.